Disclaimer: We are shareholders of Argentex.

Elevator pitch:

Argentex delivers tailored foreign exchange (“FX”) advisory and execution services to UK corporates engaging in non-speculative, commercial currency transactions. As a riskless principal broker, the company only acts as an intermediary and makes money on the spread between the rate it executes the trade at and the one passed on to the client. It has a market capitalization of GBP140m and generates GBP29m of revenues from spot, forwards and options. Banks have 85%+ of the market today but this is eroding fast: FX is a marginal vertical for them – most of their money is made on equity/debt raise and M&A – and therefore client service is poor (FX desks are cut every year) and pricing uncompetitive (150 bps for a spot trade vs. 20bps at Argentex). As one of the best capitalized independent FX broker in the UK (GBP20m net cash as of Sept-20) and with a large, highly incentivized salesforce, we think Argentex can disproportionately benefit from this market share shift and grow at 25%+ p.a. for at least the next 5 years. Argentex’s economics are excellent, with 40%+ EBIT margins and 90%+ ROIC (adjusted for cash required for collateral purposes during the year). With little need for capital reinvestment, we think the company has a clear path to a 29% FCF CAGR, reaching GBP 38.8m by March 2026. Applying an 8% FCF to EV yield leads to an intrinsic value of GBPx 510 per share, or a 33.1% IRR on capital invested from current levels (GBPx 122 per share). Additionally, the company has just entered the European and Australian markets, providing for material upside optionality if it can replicate its model successfully. Finally, insider ownership is high with the three Founding Partners owning 25% of the company. They have significant knowledge and experience in FX markets and are all involved in the day-to-day operations of the business (2 co-CEOs and 1 Managing director).

1- Company Description & Addressable Market

While 64% of notional FX traded was spot and 36% was forwards, the

latter carries higher spreads (c.30 bps vs. spot at c.17bps) and therefore sales

are more balanced with a split between spot, forwards and options at 46%, 48%

and 6%, respectively.

Additionally, it is important to understand that Argentex only acts

as a pure intermediary for its clients and therefore does not actively trade on

the market nor make directional bets on currencies. It only makes money

from the spread between the rate it executes the trade at its institutional

counterparty and the rate it passes on to the client.

How big is

the UK FX market and what is the relevant TAM for Argentex?

Establishing

an accurate addressable market is difficult as the company targets a subset of

the UK corporate world. However, the following sets of numbers directionally show

how big the market is and highlight the large runaway of market share gains

Argentex enjoys.

A recent

survey from the Bank of England[1]

stated that the average daily volume of FX traded through London is over GBP2.0

trillion of which c.GBP670m is non-interbank spot and forward trades. This same survey estimates that c.85% of

UK SME and corporate clients continue to use clearing banks as their main

provider of foreign exchange services. As Argentex’s average daily trading

volume is GBP46m, this would represent a global market share of 0.007% or

0.046% of the non-bank sub-segment.

However, the

ONS estimates that the total value of goods and services imported and exported

to and from the UK in 2019 was c.GBP1.4tn, implying a daily volume of GBP5.4bn.

We believe that the ONS statistic represents a better proxy of Argentex’s TAM

as the Company only deals with clients that engage in commercial FX

transactions. As a result, we estimate that Argentex’s market share is

c.0.9% (GBP46m of average daily trading volume in 2019).

2-

Moat

and Financial Snapshot

We believe that Argentex has 5 key attractions for clients, which put

together will allow the company to disproportionately benefit from the shift

away from banks and retain its clients.

Ø Unmatched Service and Proactivity

The typical Argentex client or prospect does not have a treasury

department and its CFO/treasurer is actively looking for service or advice. Simply

put, they like to speak to someone before putting on a GBP10m trade. Banks do

not fit the bill as they typically offer poor service (FX desks are

understaffed and the first victim of cost cutting initiatives) and cannot provide

advisory services (banking regulations). On the other hand, Argentex only

has 1,200 clients and can therefore approach them on a case-by-case basis and provides

a degree of service and proactivity that is unmatched[2].

This high-level service results in many clients using Argentex as their sole FX

providers. We expect that for clients using multiple providers, this will

result in wallet share gains over the long-term.

To this end, Argentex decided not to operate a 360 model (like most alternative FX providers). Instead, the salesforce is only focused on new customer acquisition while traders oversee the day-to-day relationship with existing clients. Also, we very much appreciate Argentex’s remuneration policy in that regard and think it fosters both a strong sense of loyalty as well as client-centricity among its employees:

- The salesforce is paid 10% to 17% (depending on new business acquisition targets) of the revenues generated by an acquired client over the lifetime of the business relationship;

- Traders are paid 10% of the revenues generated by a client.

Overall, Argentex attracts clients that predominantly value the

company’s advisory services and proactivity. For this reason, we believe that

pricing pressure is unlikely as the client perceives the spread as compensation

for the advisory service, not only for the execution. Additionally, this

protects Argentex from fintech FX startups, who propose a do-it-yourself

approach to SMEs. We do not believe that “unsophisticated” clients will want to

trade forward contracts by themselves or trade even a couple of millions worth

of GBP/EUR/USD in spot contracts without getting some advice first.

Ø Low Prices

We estimate that on top of a better service, customers switching to

Argentex can cut their FX costs 5 to 10-fold. Indeed, banks generally

charge between 100bps and 200bps on spot transactions whereas Argentex only charges

c.20bps. A similar difference holds true for forwards. Interestingly,

prospective clients generally do not know the extent of banks’ spreads since

pricing is very opaque and this is a key element of the sales pitch. For them, switching

to alternative FX providers such as Argentex can yield significant and

immediate improvement in margins.

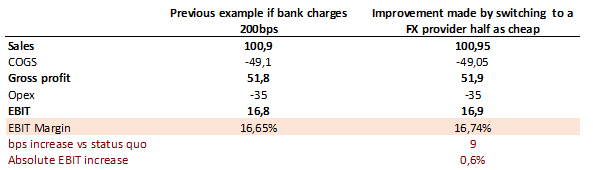

Case Study (1/2):

Let us take a UK corporate with a 15% EBIT margin that exports 50% of its goods

and imports 50% of its raw materials from Europe. Assuming all FX transactions

are made with spot contracts, the following table shows that switching from

banks charging 100bps and 200bps to Argentex’s 20bps will improve margins by 74bps

to 165bps and increase EBIT between 5% and 12%.

Trust is key in this business given the critical nature of the service

provided and while the significant savings entailed by the first switch to an

alternative FX provider more than justify the “risk”, we believe that the

rewards from switching to a cheaper alternative, once pricing is already at

20bps, is immaterial and clients are therefore extremely sticky.

Case Study (2/2):

The following table shows the impact on margin and EBIT of a switch from Argentex

to another alternative FX provider charging only 10bps.

Ø Strong reputation and highly engaged salesforce

As we mentioned previously, trust is key and Argentex benefits from a strong reputation and a long-standing track-record of operations. In addition, we believe that its listing (IPO in June 2019) significantly improved awareness among prospective clients and that it makes them more inclined to deal with Argentex since they can check the company’s financial health. Interestingly, Argentex’s institutional counterparties decreased their initial collateral requirements following the IPO as they gained more confidence in the company’s financial position.

Moreover, Argentex puts a big emphasis on the quality of its sales force

because while lower prices and good service are part of the client’s acquisition

equation, the real tipping point always comes down to the salesman. For this

reason, the company hires 10 new graduates every 6 months that it tightly integrates

within its experienced sales force. This allows best practice sharing among the

new hires and a training from the ground up to the Argentex-way. Indeed, co-CEO

Carl Jani stresses the need to “be genuine” and to take pride in the value the

product brings to the client. As a result, the company strongly discourages “product-pushing”

and will only sell to the client what it needs, and not more exotic (and higher

spread!) products.

Ø Fortress Balance Sheet

The company was GBP13m net cash at H1’21 (Sept-2020), excluding our

estimate of the cash required for collateral purposes. We believe this is a

strong attraction to clients wanting to avoid FX providers that could go under

pressure while they have outstanding contracts with them.

Additionally, FX trading requires cash on the balance sheet for

collateral purposes and this acts as a significant barrier to entry. It takes

around GBP2m of cash to trade GBP3bn of FX (our estimate following conversation

with management). Replicating Argentex current GBP12bn footprint would therefore

require at least GBP8m of cash on the balance sheet.

Importantly, the comfortable cash position allows the company to take

advantage of volatile market activities when other providers retreat. Argentex

can then step up to underwrite more transactions and therefore gain market

share. Case in point: March was the

best performing month of 2020 when Argentex collected GBP5m of revenues versus

GBP1.5m in August (GBP29m for the entire year).

Ø Regulation

While the industry is not heavily regulated, getting certifications is

still an additional barrier to entry (time and energy consuming). Alternative FX

providers need to be approved by the FCA in the UK as well as comply with MIFID

2.

To recap, these 5 key attractions constitute a powerful cocktail that

translated into 30%+ p.a. top line growth over the past 5 years, 40%+ EBIT

margins and triple digit returns on capital employed (adjusted for the cash

required for collateral purposes).

3-

A

Management Team with Skin in The Game

The three founding partners own 25% of the company, representing GBP34.0m at GBX 122 per share.

They are involved in the day-to-day operations of the business and have

extensive experience of FX markets. Additionally, Sir John Beckwith’s

Pacific Investments Group owns 12.5% of the capital, after having funded

and backed the group since its creation in 2012. The company is currently chaired

by Sir Digby Jones, a British businessman and politician who has served as

Minister of State for Trade and

Investment between 2007 and 2008.

Management has gone through the Euro crisis, Brexit and now COVID so it understands

very well that the FX business can be volatile in the short-term. It therefore prefers

to spend its time focusing on how to best position Argentex for the next 5-10 years.

This focus is rather evident from two main decisions taken this year:

-

Management

decided to move into a bigger office and to keep hiring its salesforce cohort

last summer, even if it puts profitability under pressure for the year;

-

Management

rejected many trades from prospects and clients that were not considered strong

enough to withstand COVID. Doing so would have helped increase sales (and the

share price) in the short term but at the cost of putting Argentex in jeopardy

in the longer-term if the client went under.

In an industry where risk management and discipline are paramount, we therefore

feel in particularly good hands with Argentex’s owner-operator founders.

4-

Valuation

We expect the company to keep taking market share from banks in the

years to come, which should largely support the company’s ambition of c.25-30%

top line growth per year. This leads us to sales of GBP102m revenues in 2026

(23.4% CAGR) on FX volumes of GBP45.7bn. This would imply a 3.3% market share

based on the ONS numbers assuming no growth in the economy by 2026. The cost

base is almost entirely variable (commissions account for 65% of total OPEX)

and we therefore expect EBITDA margins to grow from 48.0% to 49.6% during the

period and absolute EBITDA to reach GBP50.7m (the margin declines in 2021 as

the activity temporarily retreats while Argentex continues to recruit new salespeople

and moves its HQ to a bigger location).

Argentex owns its technological IT platform and does not capitalize much

R&D OPEX so we expect CAPEX to stay at around GBP2.5m per year. At the

Company’s 19% tax rate, this leads to a free cash flow pre and post-interest

(there is no debt) of GBP38.8m (28.7% CAGR).

Applying a conservative 8% FCF to Enterprise Value gives us a target

Enterprise Value of GBP485m in 2026. Due to its high cash conversion profile,

we expect Argentex’s net cash position to reach GBP139m by 2026, of which GBP94m

will be available to shareholders (we consider the other GBP45m as restricted

cash used to fund potential collateral payments). This leads to a target

Market Capitalization of GBP578m, or GBPx510 per share. We therefore expect an

investment at current prices of GBPx122 to generate a 33.1% IRR over the next 5

years.

5- Risks

Given the highly concentrated nature of our portfolio, we focus a lot on

what could go wrong and how it could lead to permanent loss of capital, which

is why we spent a significant amount of time considering the key risks related

to this investment.

Bankruptcies of top end-customers

-

As a

riskless principal broker, the company is not exposed to customer bankruptcy

per se, but to the following scenario: a big customer going bankrupt with an

ongoing forward trade and at the same time an adverse move in the underlying currency.

If this happened, Argentex would immediately ‘cancel’ the trade by booking an

equal and opposite trade with its institutional counterparties. Argentex would however

be on the hook for the losses created by the adverse currency move.

Ex: A client with a GBP100m forward contract goes

bankrupt. The underlying currency moves against the client by 10% on the same

day. Argentex ‘cancels” the trade as described above and limits further damage.

However, the company is on the hook for c.GBP10m, i.e. the GBP100m notional

times the adverse currency move (10%).

- Risk

management is therefore at the core of what the company does. This starts pre-trade, with not chasing what

Carl Jani refers to as “dirty revenues” and be willing to sacrifice short-term

financial performance for the long-term health of the business. Management’s first

question when looking at a deal is “does this have the potential to hurt us?”. Additionally,

a lot of time is spent assessing the creditworthiness of each client and the

company will require up-to-date financials from them when they want to put on a

big trade. The company also has strong risk parameters regarding its exposure

to a limited number of clients or industries.

Ex: During the summer of 2020, it could have done a deal with a retailer

and taken £2m for £200m underlying currency, which would have shown stronger H1’20

results. It did not and the retailer is now bankrupt. The company would have

been in a more precarious situation if it accepted the deal.

- Post

trade, Argentex will do daily sensitivity analysis on the top 20 “most at risk”

clients and simulate diverse currency scenarios. It will also look at its

overall currency exposure to see where traders can be more lenient on

collateral requirement or on the contrary where they need to be strict.

Damage of reputation due to poor client services or KYC procedures

- As

explained previously, reputation is paramount in this industry and one of the

competitive advantages of independent FX providers is better client service

compared to institutional banks;

- Poor

client services arising from incorrect trade execution, human error, trader’s

unavailability to answer queries on time could have a severe negative effect on

the company’s reputation and on its activity. Indeed, as the famous saying goes

“it takes 20 years to build a reputation and five minutes to ruin it”;

- Argentex

is still a nascent company in this industry and sometimes gets referenced to

other clients by word of mouth. Even a tiny portion of clients being

unsatisfied can have a snowball effect and therefore impact the growth of the

company;

- In

parallel, poor KYC procedures leading to some client bankruptcies, while

limited, can spread negative sentiments (even unjustified) around the solidity

of the business.

Poor integration of new recruits

-

Because the

salesforce is key in bringing in new clients, recruits need to be trained and reach

the skill level of the experienced salesforce for the business to achieve its

growth targets. Indeed, as the following charts shows, as recruits gain

experience, they become better at acquiring clients;

-

However,

training from scratch a new batch of recruits every 6 months (a work done by

the co-CEO and the experienced salesforce) requires time, energy, patience, and

salary expenses without the guarantee of success. As a result, it can disturb

the work organization of experienced team members as they need to allocate time

between training and sourcing new prospects;

-

While we

welcome the quasi-constant arrival of fresh and motivated young graduates, we

also consider it as a risk that Argentex will need to take into account if it

wants to optimize its growth prospects without impacting the current solidity

of its team.

Appendix 1

Some examples from our research:

-

Traders

usually find out the rates at which clients are interested in or the day

clients like to trade and call them before they have to;

- Argentex

will sometimes charge less than it could on a specific trade to keep a good

relationship (whereas bank pricing is largely based on mechanical grid prices);

-

Flexibility

over settlement payment: bank will charge corporates a lot if they do not pay

at settlement whereas Argentex will be more flexible;

- Argentex

will also be more flexible around the corporate structure: SPV for instance are

rejected by banks for FX services although they are backed by massive PE firms.

[1] Link to the press release: https://www.bankofengland.co.uk/markets/london-foreign-exchange-joint-standing-committee/results-of-the-semi-annual-fx-turnover-survey-october-2018

[2] See Appendix 1

Is there a reason to get excited about this now?

ReplyDeleteIs Record Plc a suitable peer for Argentex?

ReplyDeleteRecord Plc is experiencing a strong re-rating right now, while Argentex is not impacted so far.

Is Record Plc a suitable peer for Argentex?

ReplyDeleteRecord Plc is experiencing a strong re-rating right now, while Argentex is not impacted so far.

Hey man, thanks for the write up. Our small partnership has invested in AGFX.

ReplyDeleteWhat are your takes on those:

- bad press about Henry

- Digby has missed compliance and a former company, where he was sitting in the board, wenn bankrupt after a fraud

- did you speak to employees of alpha fx about differences? There are some things I got concerned about.

You find my write up here: http://investmentideen.com/?p=338&lang=en

DeleteWhat differences did you find when you spoke to employees? I see no reason why AGFX should trade at such a discount to alpha

DeleteSeeing the latest investor call, some thoughts from me:

ReplyDeletePassing mention of high attrition rate among sales staff, probably the driver for the 'pod' reorganisation they trialled.

Detail on software in the appendix was quite impressive, personal experience tells me that really high quality system integration like they claim is a massive, massive driver of productivity, and very difficult for rivals to imitate.

The news from Netherlands not great - my read is that they are having to reinvest in their online offer because the old high service model (where their competitive advantage lies) isn't what the Dutch wnat.

Overall - pretty positive set of results - I added after the investor call.

당신의 블로그의 다음 업데이트를 계속 체크 아웃하기를 기대합니다.

ReplyDelete외환거래

Met Glass / Glass solar modules and panels

ReplyDeleteGlass glass solar module is a long lasting and ultra resistant to any weather conditions Building Integrated Photovoltaics solution. BIPV solar panels can be used as an additional power source and alternative material in architecture to achieve future design for a comparable to standard materials price.

https://metsolar.eu/